Reporting and Analyzing Shareholders' Equity

Corporate form of Organization

Characteristics of a corp

Shareholder rights

Share issues considerations

Share capital

Accountign for common and preferred shares

Accounting for Dividends and Stock splits

Cash and stock dividends

Stock splits

Comparsion of effects

Presentation of shareholders' equity

Statement of financial position

Statement of changes in equity - IFRS

Statement of retained earnings - ASPE

Summary of shareholders' equity transactions

Measuring corporate performance

Dividend record

Earning performance

The Corporate form of organization

A separate legal entity

Separate and distinct from its owner

Has most of the rights and privileges of a person

May be public or private

Public

Many shareholder, shares are publicly traded and held

Private

Few shareholders, shares are closely held and not traded

Characteristics of a corporation

Separate legal existence

Limited liability of shareholders

Tranferable ownership rights

Ability to acquire capital

Continous life

Corporation management

Government regulations

Income tax

Advantages and Disadvantages of a Corporation

Share Issue Considerations

To raise capital, the corps sells ownership rights in the form of shares

Shares can be divided into different classes

Usually referred to as common shares and preferred shares

Common and preferred shares for share capital

Ownership rights are specified in article of incorporation or in by-laws

Rights in voting, dividends, liquidation

Authorized shares

Max amount of shares corp allowed to sell

May be limited or unlimited

Not recorded; disclosed only

Issues shares

Number of shares sold

Legal capital

Share cpaital cannot be distributed to shareholders, unlike retained earnign, which can be dsitrubted as dividends

Fair Value of Shares

First issue normally through initail public offering

Share price is set by the company

Once issued, shares of publicly held companies trade an organized exchanges

At price per share established between buyers and sellers

Fiar value of shares

Share price is determined by market forces

Issuing Common Shares

Share capital

The amount that shareholders have paid to the corp for their shares

Shares are usually issued for cash

Dr.Cash

Cr. Common Shares

Shares can be issued in exchange for services or noncash assets

IFRS: Record at cash equivalent price

ASPE: Fair value of shares given up or fiar value of consideration received

Reason to Repurcahse Common Shares

Distribute Cash to shareholders

Increase trading on securityies markets

Reduce number of shares issued per share and return on common shareholders' equity

Buyout hostile shareholders

Have share available for compensation or other uses

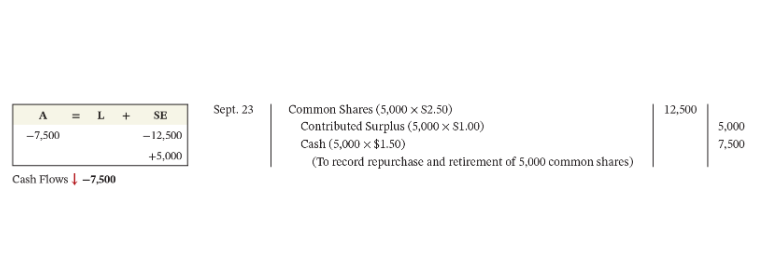

Repurchase of Common Shares

Repurcahsed shares are a corp's own shares wither common or preferred that had been previously issued and later reacquired by the corp

Normally retired and cancelled

Removed from the share capital account

Can also be held as treasury shares, for future resale, in limited circumstances

Only in some provincesand foreign jurisdictions

Steps

Remove cost of shares from share cpaital account

Record the cash paid

Reocrd the gain or loss on repurchase

Repurchase Below Average Cost

Screen clipping taken: 2024-03-18 8:38 PM

Repurchase Above Average Cost

Screen clipping taken: 2024-03-18 8:39 PM

Preferred Shares

Preferred shares have contractual provisions that give them priority over common shares

Usually do not have voting rights

Accountign for preferred ahres similar to common shares

Screen clipping taken: 2024-03-18 8:39 PM

Preferential Features of Preferred Shares

Specified dividend rate

Dividend preference

Preferred shareholders must be paid dividends beofre any paid to common shareholders

Cumulative divididends in arreats

Liquiations preference

Other preferences

Conversion privilege

Redeemable/callable (company option)

Retractable (shareholder option)

Dividends

A pro rata (equal) distribution of a portion of a corps retained earnigns to its shareholders

Cash dividends are most common

A distribution of cash to shareholders

Stock dividends may also be issued

Cash Dividends

For a cash dividend to occur, a corp must

Meet a 2 part solvency test CBCA and

Effect a formal declaration of dividends by boards of directors

3 important dates in connection with dividends

Declaration date

Date the board of directors formally authorizes the cash dividends

Commits the corp to a binding legal obligation

Example: declartion on Dec 1 of 1 50 cent per share quaterly cash dividend on a 2 dollar preferred shares

Screen clipping taken: 2024-03-19 6:11 PM

Record date

Date ownership of shares is determined for divided purposes

No journal entry required

Payment date

Date dividends are paid to shareholders

Example: pay date is jan 20

Screen clipping taken: 2024-03-19 6:12 PM

Stock Dividends

Cash dividends is paid in cash, whereas

Stock dividend: distributed (paid) in shares

Fair value on date of declartion is assigned to the stock dividend shares

Same 3 dates as cash dividends

Stock dividend does not change assets, liabilities or total shareholder's equity

Purposes and Benefits of Stock Dividends

Satisfy shareholders' dividend expectations without spending cash

Increase marketability of the shares

Increases number of shares and decreases market price per share

Reinvest and restrict a portion of shareholders' equity

Unavailable for future cash dividends

Examples

Assume that 50, 000 common shares

Balance of 500,000 in common shares account and 300,00 in retained earnings

A 10 percent stock dividend, 5,000 common shares (50,000*10 percent) would be issued

Amount debited to dividends declared account is 75,000 (5,000*$15)

15 is market price of the shares

Stock Dividends Entries

Screen clipping taken: 2024-03-19 6:17 PM

Effect of stock dividends on shareholders' equity

Screen clipping taken: 2024-03-19 6:17 PM

Stock Splits

A stock split involves the issues of additional shares to shareholders according to their percentage ownership

Like a stock dividend but much largers

Primary purpose is to increase marketability of shares by lowering share price

A stock split has no effect on total share capital, retained earnign, or total shareholder's equity

Market value of the shares will decrease roughly proportionately to the split

Not jounrnalized

Screen clipping taken: 2024-03-19 6:19 PM

Comparison of Dividends and Stock splits

Screen clipping taken: 2024-03-19 6:19 PM

Presentation of Shareholder's equity: Statement of Financial position

Share capital and contributed surplus

Share capital: preferred and common shares

Contributed surplus: amounts contributed from repurchasing and retiring shares

Retained earnigns

Cumulative net incomes since incorp

Annual net incoem is added ; net losses and dividends declared are deducted

A portion may be restricted and therefore unavailable for dividends

Accumulated Other Comprehensive Incoem (IFRS)

Other comprehensive income reported ONLY under IFRS

Other companies comprehensive income OCI includes certain gains and losses that bypass new income such as revaluation gains and losses of property, plant, and equipment using the revaluation model

Accumulated other comprehensive income AOCI is the cumulative change in shareholders equity

Starts with opening balance and is increased (decreased) by other comprehensive income each period

Comprehensive Income

Total comprehensive income includes net income (loss) and other comprehensives income (loss) OCI

Screen clipping taken: 2024-03-19 6:23 PM

Statement of Changes in Equity IFRS

Discloses changes in total shareholders equity for the period, including

Share capital

Contributed surplus

Retained earnigns

Accumulated other comprehensive income

Required under IFRS

Stateent of Retained Earnigns ASPE

For private companies who have a simpler share sturctures and few share transactions

Shows the amounts and changes in retained earnings during the period

Beginning retained earnign amount +net income - dividends declared = ending retained amount

Required under ASPE

Measuring Corp Performance

Dividend record

Payout ratio

Measures the percentage of progit distributed in the forms of cash dividends to common shareholders

Payout ratio= cash dividends declared/ net income

Higher is better if investor looking for more income

Investors looking for share price appreciation would look for lower payout ratios

Dividends ratio

Measures the profit generated by each share, based on the market price of the shares

Dividends = Dividends decalred/ market price per shares

Higher is better for income

Lower is better for price appreciation

Earnings performance

Basic earnign per share

Return on common shareholders' equity

Basic Earnings per Share (EPS)

Measures the income earned by each common share

Basic earnings per share = income available to common shareholders/ weighted average number of common shares

Income to common shareholders = net income less perferred dividends

Increased EPS over prior years indicate improved performnance

Not comparable between companies

Weighted average number of common shares

Shares issued during the year x the fraction of the year they are out standing

Example: oct 1 - 3/12

Screen clipping taken: 2024-03-19 6:42 PM

Return on Common shareholders' equity

Measures the company's profitability from the shareholders' viewpoint

How many dollars were earned for each dollar invested by common shareholders

Commons shareholders' equity

= total shareholders' equity - legal capital of preferred shares

Return on common shareholders' equity = income available to common shareholders/ average common shareholders' equity

Higher is better

No comments:

Post a Comment