Statement of Cash Flows

Reporting of cash flows

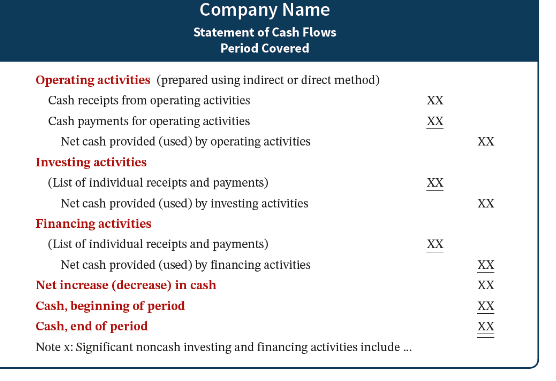

Classification, format and prep of statement of cash flows

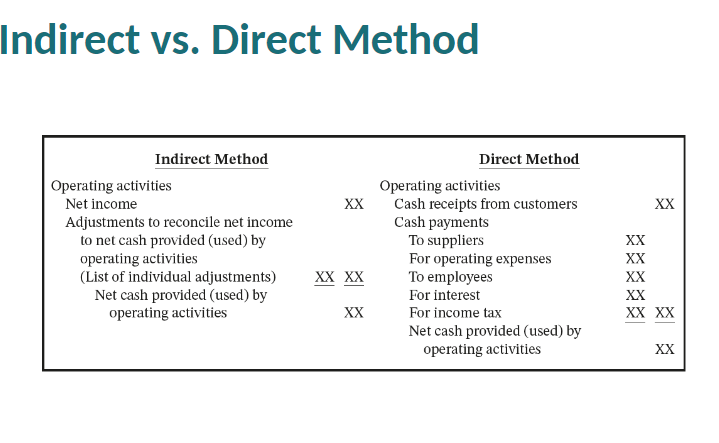

Indirect method

Operating activities section

Prep of operating activities section

Summary of conversion to net cash provided (used) by operating activities

Investing activies

Prep of investing section

Financing activitie section and completion of statement of cash flows

Prepparation fo financing activities section

Completion of statement of cash flows

Using cash flows to evaluate a company

Corporate life cycle and cash flows; free cash flow

Direct method

Operating section

Cash recepts and payment

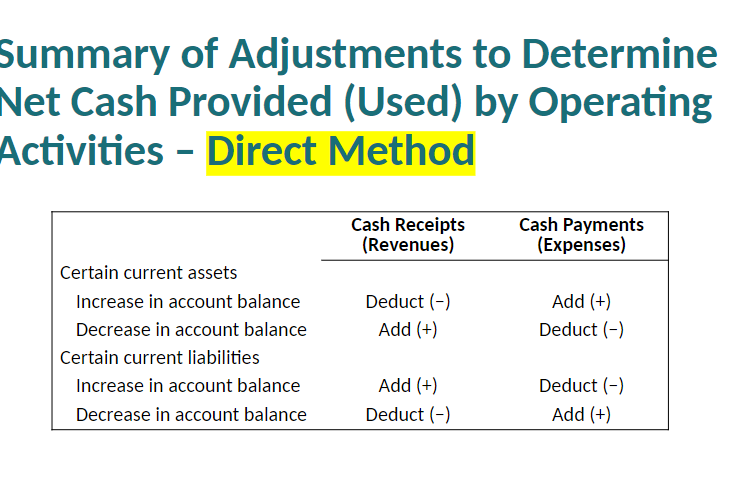

Summary of conversion to net cash provided by operating activities

Purpose of statement of cash flows

Helps users assess a company's ability to generate cash from its operating acitivites

How the company received and used other cash flows regarding investing and finacing activities

This is useful in determing a company's ability to generate future cash flows

Investing and finacing transactions during the period, and effect upon capital structure

Making comparsions with other companies

Definition of Cash Classification of Cash Flows

Cash may include cash equivalents

Short term, highly liquid investments that have insignificant risk and are readily ocnverted to cash within a short period of time

Cash receipts and payments are classified into 3 categories

Operating

Investing

Financing

Operating

Related to a company's principlal income-producing activites

Activities relate to cash effects of transactions that create revenues and epxneses that enter into determination of net income

Includes relevant noncash curent assets and current liabilities on that statement of financial postion, where the rlated account is a statmet of income accoutn

Investing

Related to the aquistion and disposal of non-current assets

Purcahsing and disposing of

Long lived assets and investments hot held for trading

Generally includes non-current asset items on the statement of financial position

Financing

Related to changes in a company's debt and equity, including

Obtaining cash from issuing debt and repaying the amounts borrowed

Obtaining cash from selling common and preferred shares and paying devidends

Generally includes non-current liabilities, and shareholders' equity items

Significant noncash activities

If it does not affect cash, do not report in statement of cash flows

Report in spearate note to the financial statements

Examples

Issue of shares to purchase assets or to reduce liabilities

Conversion of debt into equity

Exchange of property, plant and equipment

Screen clipping taken: 2024-03-25 7:15 Pm

Indirect vs. Direct Method

Screen clipping taken: 2024-03-25 7:18 PM

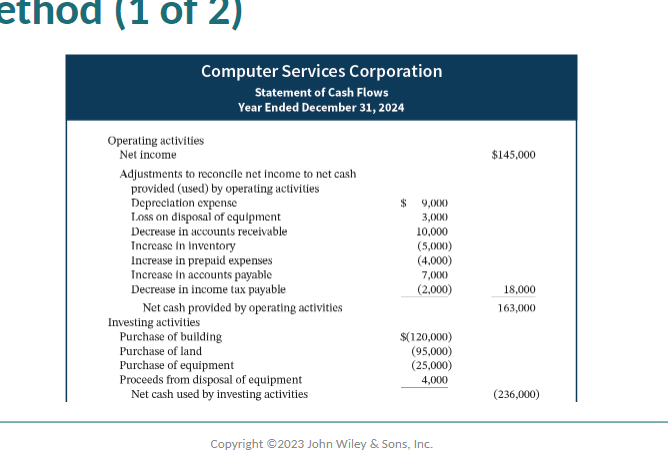

Step 1: Operating Activities

Determine the net cash provided by operating actviities by converting net icnome form an accrual basis to cash basis

Conversion may be done by either indirect or direct method

Both arrive at same aomount

Most companies favour indirect method

Easier to prepare

Reveals less info

Prepare the operating activities section using the indirect method

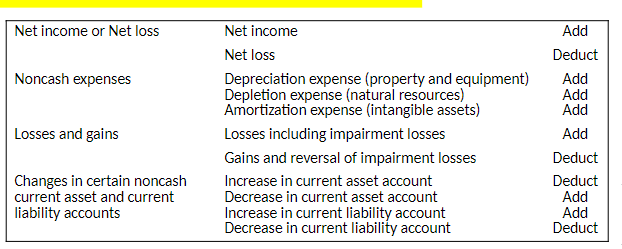

Start with net income and add or deduct items not affecting cash to arive at net cash provided by oeprating acitivities

Add non cash expenses suhc as depreiation and losses

Subtract non cash gains

+ Decreases in current asset accounts and increases in current liability accounts

- Increases in current asset accounts and decreases in current liability accounts

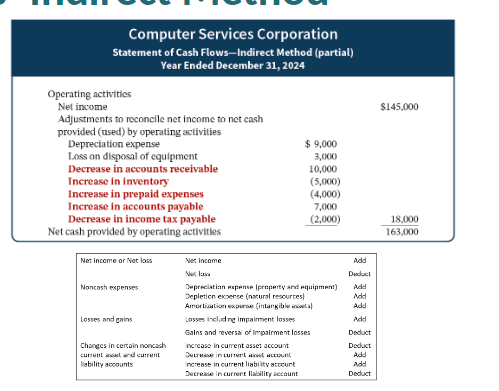

Summary of Adjustments to Determine Net Cash Provided by operating activities -indirect method

Screen clipping taken: 2024-03-25 7:25 PM

Net cash provided by operating activities -indiect method

Screen clipping taken: 2024-03-25 7:26 PM

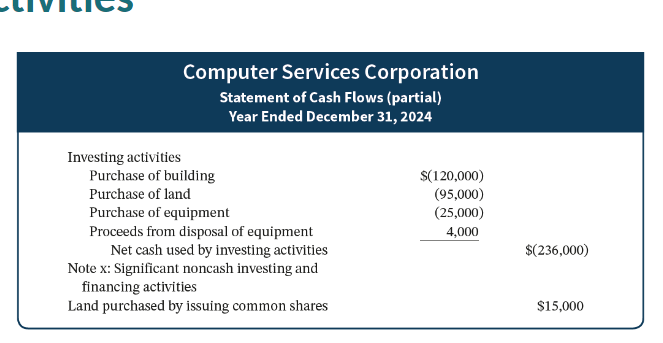

Step 2: Investing Activities

Measure cash flows relating to non-current asset accounts; long-term investments; propty , plant and equipment; intangible assets

Reported the same under both direct and indirect methods

Assets acquisitions are uses cash;disposals are sources of cash

Depreciation expense is a noncash charge

Net Cash provided by investing activities

Screen clipping taken: 2024-03-25 7:30 PM

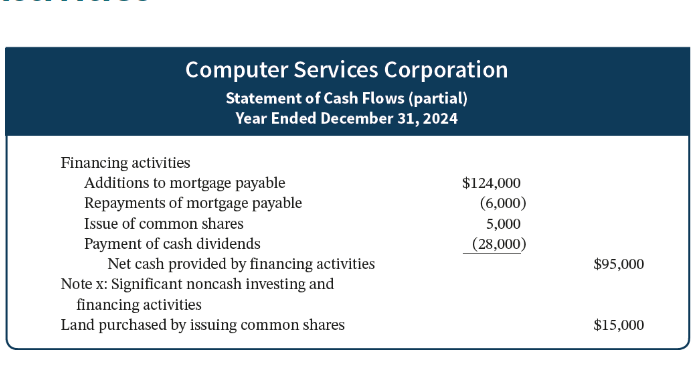

Step 3: Financing activities

Determine the net cash provided by financing activities by looking at changes in non-current liabs and equity accounts

Changes to notes, loans and mortgages, and bonds payable for cause of change

Share capital and retained earnings accounting for changes and cause

Profit is reported in the operating activities section

Net Cash Provided by Financing Activities

Screen clipping taken: 2024-03-25 7:32 PM

Step 4: Complete the statement of cash flows

Complete the statement by combing the operating and all other sections

Determine increase(decrease) in cash for the period

Ensure ending cash balance agrees wo that reported on statement of financal positon

Identify any non cash discloseures

x

Statement of Cash Flows Indirect method

Screen clipping taken: 2024-03-25 7:35 PM

Screen clipping taken: 2024-03-25 7:35 PM

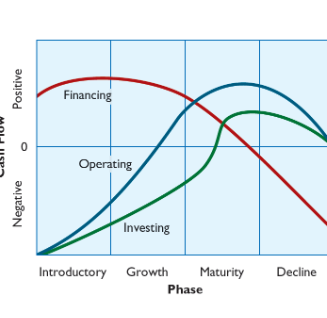

Using Cash Flows to Evaluate a Company

Corporate Life cycle and Cash flows

4 Phases:

Intro

Growth

Maturity

Decline

Helps to understand a company's cash flow from activities

Screen clipping taken: 2024-03-25 7:42 PM

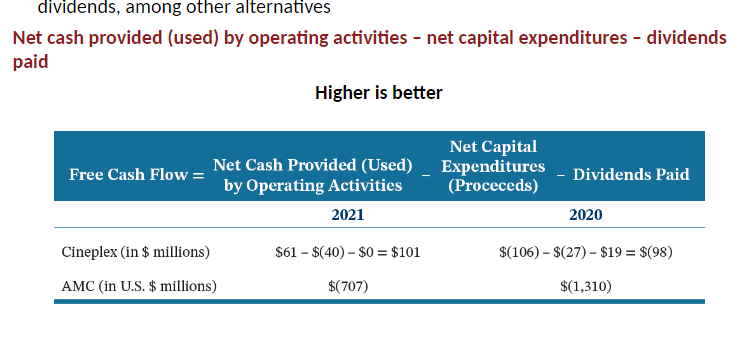

Free Cash Flows

Measures discretionary cash flow remaining for operating activities available to use to expand operations, reduce debt, go after new opportunities, or pay additional dividends, amoung other alternatives

Screen clipping taken: 2024-03-25 7:43 PM

Prepare the operating activities section using the direct method

Details cash receipts and payments

Similar to indirect method

Adjusts statement of income from accrual basis to cash basis in order to arrive at net cash provided by operating activities

Indirect adjusts total net income.

Direct adjusts individual revenue and expense item in the statement of income

Cash Receipts from Customers

The relationship between cash receipts from customers, revenues from sales, and changes in accounts receivable and deferred reveue is

Screen clipping taken: 2024-03-25 7:48 PM

If other cash receipts, these must be adjusted for any receivable amounts as was done above

Cash payments to suppliers

The relationship between cash payments to suppliers, COGS, changes in inventory, and changes in accounts payble:

Screen clipping taken: 2024-03-25 7:50 PM

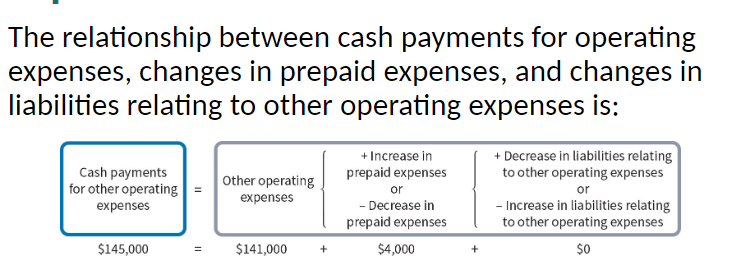

Cash payments for other operating expenses

Screen clipping taken: 2024-03-25 7:54 PM

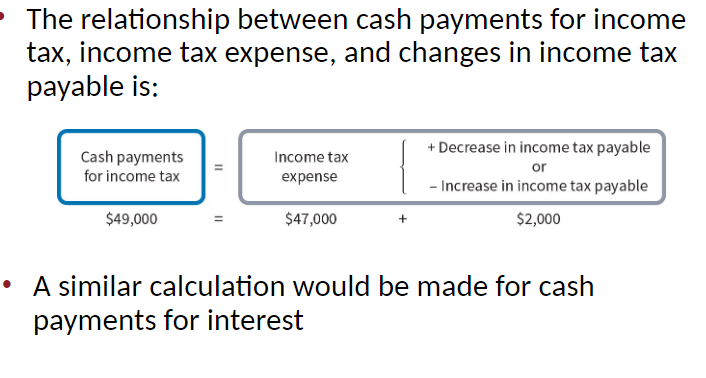

Cash payments for income tax

Screen clipping taken: 2024-03-25 7:54 PM

Screen clipping taken: 2024-03-25 7:55 PM

Screen clipping taken: 2024-03-25 7:55 PM

No comments:

Post a Comment