Performance Measurement

Comparative Analysis

Horizontal, Vertical and Ratio Analysis

Liquidity Ratios

Current Ratio, Receivables Turnover, inventory turnover

Liquidity conclusion and summary of liquidity ratios

Solvency Ratios

Debt to total assets, times interest earned, free cash flow

Solvency conclusion and summary of solvency ratios

Profitability Ratios

Gross profit margin, profit margin, asset turnover, return on assets, return on common shareholders' equity, basic earnings per share, proce-earnign P-E, payout ratio, dividend yield

Profitability conclusion and summary of profitability ratios

Limitations

Deviersications

Alternative accounting

Other income

Nonercurring items

Comparative Analysis

Making comparisions about a company's past and current financial performance and position to better determine future expectations

Financial data as well as nonfinancal info should be reveiwed

Company's mission

Strategy

Goals and objectives

Management discussitons and Analysis

Screen clipping taken: 2024-04-08 7:39 PM

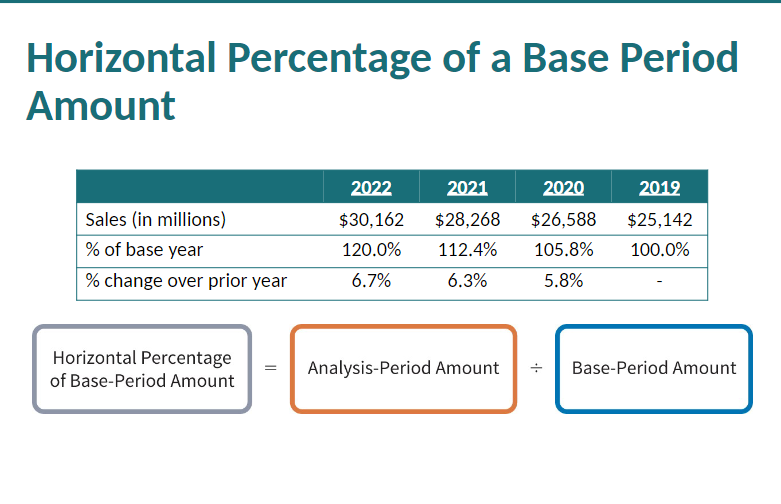

Horizontal Analysis

Also known as trend analysis

Express the change increase or decrease over time

Allows intra company comparsions

Comparing current data with other periods

Can be expressed as an amount or percentage

%of base year amount

%change for the year

Screen clipping taken: 2024-04-08 7:37 PM

Screen clipping taken: 2024-04-08 7:37 PM

Vertical Analysis

Also known as common size analysis

Expresses each item in a statement as a percent of a total amount

Comparsion of data within the statement nad within the same year

Expressed as a percentage

Screen clipping taken: 2024-04-08 7:38 PM

Ratio Analysis

Liquidity Ratios

Measure short-term ability of the company to pay its maturing obligations and to meet unexpected meeds for cash

Current Ratio

Measures short term debt ability and liability

Currents Ratio = Currents Assets/ Currents liabilities

Important to look at its components when assessing current ratio be cautious about influences of slow moving inventory

Receivables turnover

Measures liquidity receivables

Receivables turnover = Credit sales/ Average gross accounts Receivables

Average collection period

Measures number of days receivables are outstanding

Average collection period = 365 days/ receivablse turnover

Inventory turnover

Measures liquidity of inventory

Inventory turnover = Cost of Goods Sold/ Average Inventory

Days in inventory

Measures number of days inventory is on hand

Days in ventory = 365 days /inventory turnover

Solvecy ratios

Measrue the ability tof the company to surviv over a long period of time the ability to pay its total liabilities

Debt to total assets

Measures % of total assets provided financed with debt

Debt to total assets = Total liabilites/total assets

Times interest earned

Measures ability to meet interest payments as they come due

Times interest earned = Net income +Interest expense+ income tax expense/interest expense

Free cash flow

Measures cash availbale for paying dividends or expanding operations

Net cash provided by operating activities - net capital expenditures - dividends paid = free cash flow

Profitability ratios

Measure the operating success of a company for a specific period of time.

Gross Profit Margin

Measures margin between selling price and cost of goods sold

Gross profit margin = gross profit /sales

Progit Margin

Measures the percentage of profit generated by each dollar of sales

Profit Margin = Net income/sales

Asset turnover

Measures how efficiently assets are used to generate sales

Asset turnover = sales/average total assets

Return on assets

Measures overall profitability of assets

Return on assets= net income/average total assets

Return on common shareholders' equity

Measures overall profitability of shareholders' investment

Return on common shareholders' equity = net income- preferred dividends declared/average common shareholder's equity

Average common shareholders' equity = total shareholders' equity - preferred shares

Basic earning per share

Measures profit earned on each common share

Earnings per share = net incoem -

Price earning ratio

Payout raio

Dividend yield.

No comments:

Post a Comment