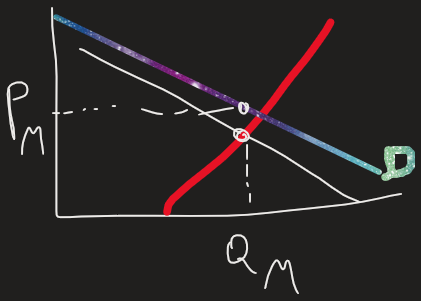

Find Pm from the demand curve at this Q

Find Pm from the demand curve at this Q

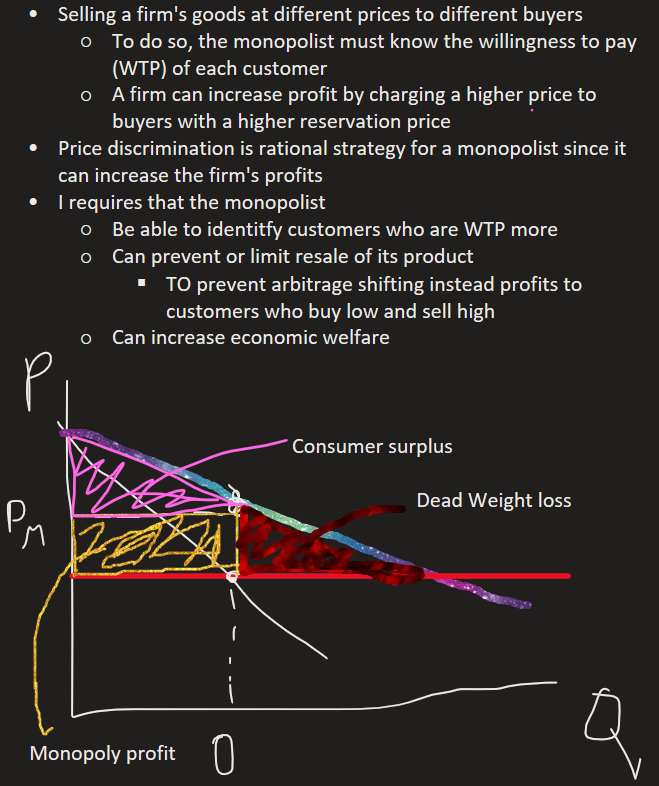

Price Discrimination

Find Pm from the demand curve at this Q

Find Pm from the demand curve at this Q

Price Discrimination

Market failure- a situation in which the market, on its own, fails to allocate resources efficiently

Externalities in the market may cause economic efficiency to be enhanced by government intervention

Since the benefit each citizen receives from having an educated community is a public good, the private market is not the best way to supply education

The government provides public goods because the freerides make it difficult for private markets to supply the socially optimal quantity

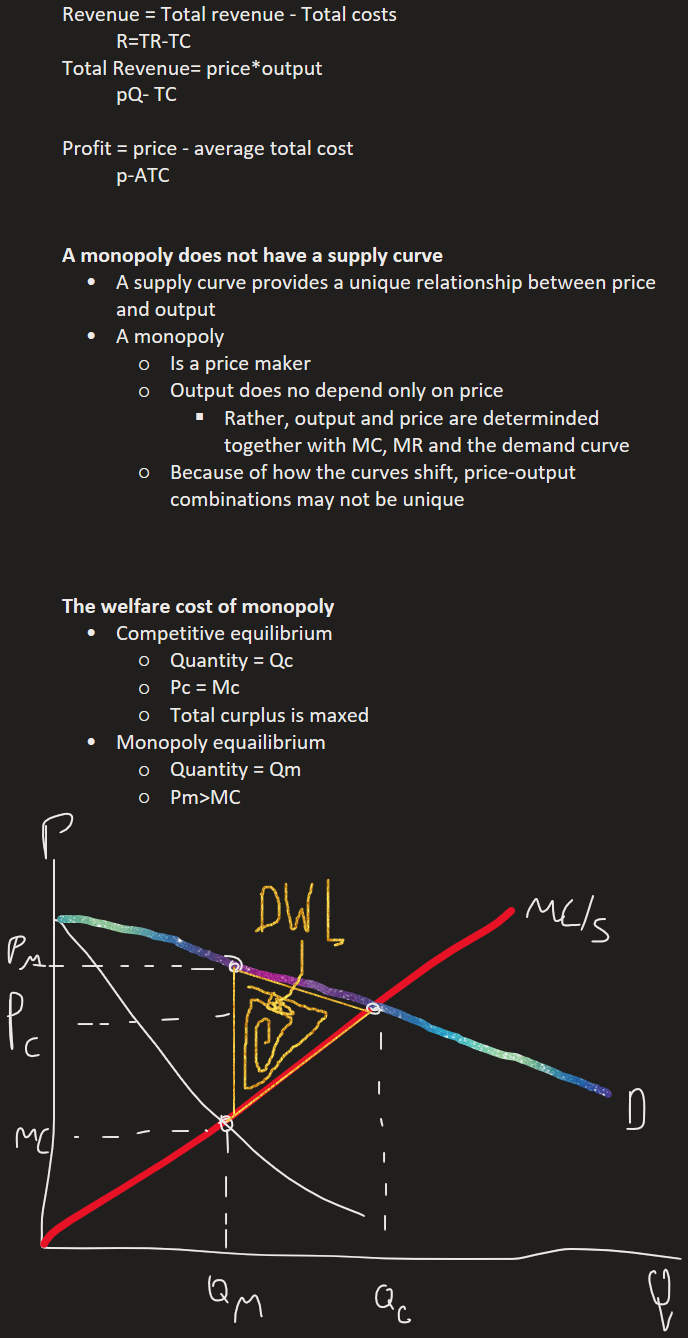

The total surplus with a tax = consumer, producer surplus, and tax revenue

If a company does not bear the entire cost of the dioxin it emits it will emit higher levels of dioxin than is socially efficient

A positive externality is a benefit to a market bystander

When the government places a tax on a product the cost of the tax to buyers and sellers exceeds the revenue raised from the tax by the government

The amount of deadweight loss from taxes depends on the price elasticity of demand and supply

The demand curve for a product reflects the value of the product to consumers

Donald produces nails at a cost off 200 per ton if she sells the nails for 500 his producer surplus is 300 per ton

A 100 dollar head tax is an example of a tax that is most economically efficient

Moving production from a high cost producer to a low-cost producer will raise total surplus

Taxes cause dead weight losses beause they prevent buyers and sellers from realizing some of the gains from tade and marginal buyers and seller leave the market causing the quantity sold to falls

In an economy, when do not have a price the government primarily ensures that the good is produced

Examples of private goods are : tennis shoes, pizza, french fires, beer

A concept of negative exnalieities can be made using a college student plays his new stereo system in the residence at 2am

In the market for a good like ice-cream cones price adjusts to balance supply and demand

Competitive Market

Full info

Everyone knows what they are trading and at what price

No info asymmetries (one party has more or better than the other)

Price takers

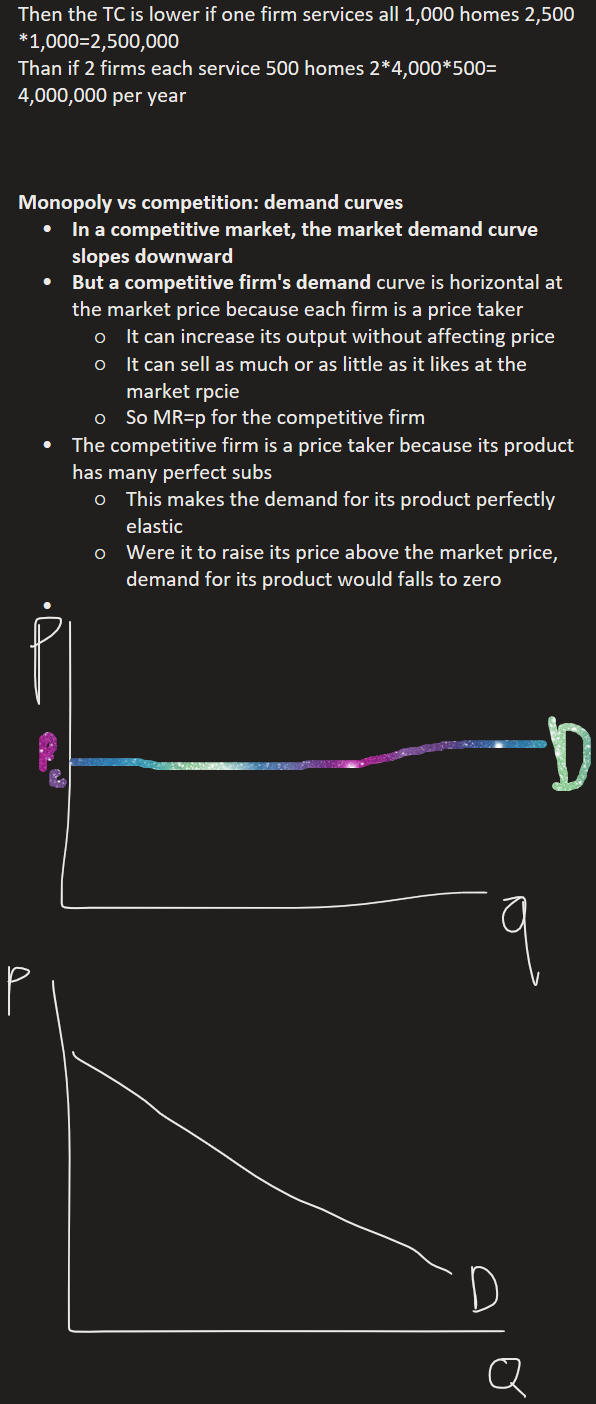

Competitive markets have so much competition that no one has the ability to affect market price. Thus all price-takers

If a buyer or seller has the ability to noticeably affect market prices, that person/firm has a market (and it's not a competitive market)

The only seller of food on a plan can charge a very high price, knowing that some people would be hungry enough to pay it.

The only buyer of food at a market at the end of the day could offer a very low price, knowing that some sellers would be willing to sell.

Participation in a competitive market places very specific constraints on a firm's ability to max profits.

Standardized goods

Goods and services have the same things and they are interchangable

In real life, goods are differentiated by qaulity, brand, or things that appeal to different tastes.

Comoodities under certain defnied things are consider standardized goods.

Free Entry and exit

Free entry and exit is not an essential condition for a competitive market, but when it does not hold, there are incentive to collude breaking the price-taking requirement

Not all markets it is as easy to entry

Revenues in a perfectly competitive market

In a perfectly competitive market, producers are able to sell as much as they want without affecting the market price.

Total revenue = Price * Quantity

Average Revenue = Total Revenue/Total Quantity

Marginal Revenue = deltaTR/deltaQ

Price does not changes

Total revenue is the price times quantity produced

Average Revenue is the total revenue divided by the quantity

Marginal revenue is the revenue generatedby selling an additional unit of a good

Notice that Price = Marginal Revenue = Average Revenue

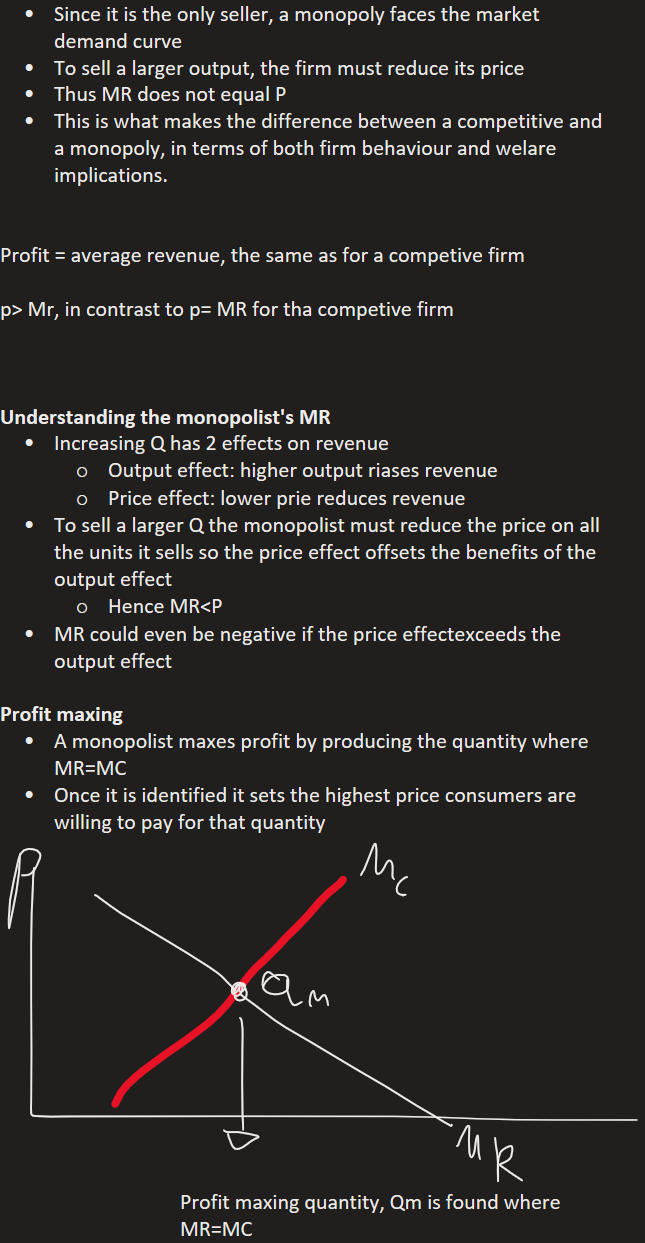

Profits and production decisions

Firms seek to max profits

In a competive market, the only choice that a pric-taking firm can make to affect profits is the quantity of outpout to produce.

The profit-max quantity corresponds to the quantity at twhich marginal revenue is equal to the marginal cost.

Profit max occurs where MR = MC for a perfectly competitive firm.

Increase production as long as MR>MC, as total profit increases as another unit is produced.

Deciding when to operate

Producing the quantity where MR = MC may not always be to the firm's advantage

When a firm shuts down production, it avoiding incurring variable costs

Fixed costs remain and are sunk in the short-run

Because fixed costs are sunk, they are irrelevant in deciding whether to shut down in the short run.

The short decision to produce depends on variable costs, not fixed costs

Shut down if P < min(AVC)

The long run decision to produce depends on total cost, since all costs are variable in the long run

Long run supply

The key difference between short run and long run is that firms are able to enter and exit the market in the long run

The process of market entry and exit causes firms in the long run in a perfetly comptitive market:

TO earn 0 economic profits in the long run

Accountingprofits are positive in the long run)

Firms operate at an efficient scale

Supply is perfectly elastic

If positive economic profits exist:

P>ATC

New firms enter to gain profits

The market supply curve shifts outward until P = ATC

Economic profits go to zero for all firms

If economic profits are negative

P< ATC

Some firms exit the market

The market spply curve shifts inward until P = ATC

Economic profts go to zero for all firms

Efficient Scale: Quantity that minimizes average total cost

Firm's optimal production : P = MR = MC

MC intersects the average total cost curve at its lowest point : MC = min (ATC)

In the long run, economic profits are 0: P = ATC

The goals of every firm

Economists assume the firm's goal is to max profits

Profit=R-E

Total revenue is the amount a firm receives from the sale of its output

Price per unit * by the quantity sold

The cost is the market value of the inputs a firm uses in production

Total costs includes one-time expenses, like buying a machine, as well as ongoing expenses, like rent, employee salaries, raw materials, and advertising

Costs are more complex and harder to calculate than total revenue

A firm's total cost is defined as

Total cost= fixed costs + variable costs.

Fixed Costs

Costs that do not depend on the quantity of output produced: They are constant as quantity increases

One time, upfront payments before production begins, like buying equipment

Ongoing payments, like monthly rents

Even if a firm produces nothing, it still incurs a fixed cost

Variable Costs

Costs that depend on the quantity of output produced

Includes the cost of raw materials, machinery, and equipment, and labour

Variable cost increases with each additional unit produced

If firm produces nothing, variable cost is zero

Explcit vs Implicit cots

The opportunity cost of something is what you have to give up to obtain it

Opportunity cost has 2 compnents: explicit costs and implicit costs

Both matter for firms' decisions

Explicit costs require an outlay of money

Paying wages to workers

Implicit cots do not require a cash outlay: rather they represent opportunities that could have generated revenue if the firm had invested its resources in another way

The opportunity costs of the owner's time

Both costs must be included to properly account for a firm's total cost.

Economic Profit vs Accounting Profit

When companies report their profits, they provide accounting profit

Accounting profit= total revenue- explicit costs

Accountants keep track of how much money flows into and out of the firm so they ignore implicit costs

As a result, accounting profit may be a misleading indicator of how well a business I really doing.

Economic profit on the other hand accounts for both explicit and implicit costs

Economic profit = accounting profit- implicit costs

Economic profit = (Total revenue - explicit costs)- implicit costs

Economists study the pricing of the production decisions of the firm, which are affected by implicit as well as explicit costs

Since accounting profit ignores the implicit costs, it's always higher than economic profit

The production function

The relationship between the quantity of inputs used to produce a good and the quantity of output that is produced given technology

Indicates what is physically possible to produce

The short run production fucntion is also called the total product function

It can be represented by a table, a graph of an equation

Example

Why is the MPL important?

When the farm hires an an extra worker:

Her costs rises by the wage she pays the worker, w

Her output rises by the MPL

The value of that extra output rises by p * MPL

p * MPL is the farmers's benefit from hiring the extra worker

Comparing the value of the extra output to the increase in costs helps the farmer decide wther she would benefit from hiring the worker

If the benefit exceeds the costs (p *MPL > w, ) hire the extra worker

Why the MPL falls

Why does the farmer's output rise by a smaller and smaller amount for each additional worker she hires?

When output I low, the MPL may increase because workers can work together and specialize in the tasks in which they have a comparative advantage

However as the farmer adds more work the additional worker, wokers will be less productive

MPL will always falls as L rises wether the fixed inpout is land or capital

This relationship between outpout and variable inputs is called the law of diminishing marginal product or returns

The marginal prodict of a variable input envenutally declines as the quantity of the inpout increases

Maginal Costs

The increase in total cost from producting one more unit

MC= deltaTC/deltaQ

Total costs= fixed costs + variable costs (FC = land, VC = Labour) = wL + FC

The MPL is increasing , MC Is falling

The MPl Is at its max, MC is at min

MPL decrasing, MC is rising

Average fixed cost = fixed cost/quantity

Average variable cost = variable cost/quantity of output

Average total cost = TC/Q

Tyrion Lannister (SHOW) Tyrion Lannister is a dwarf in the tv show Game of Thrones. His sister Cersei hates him and thinks that he is ...