Reporting and Analying Liabilties

Current Liabilities

Sales taxes

Payroll

Provisions and contingent liabilities

Statement presentation and analysis

Presentation and analysis

Liabilities

Present obligations to transfer economic resources as a result of from past transactions

Classified as current and non-current

One type of liability is financial liability these types have a contractual obligations to pay cash in future.

Currents Liabilities

Expected to be paid or settled

Within one year of the date on statement of financial posion or within the operating cycle

Thorugh payment by cash, through transfer of goods or srevices or through creation of other liabilities

Types of currents liabilities include

Bank indebtedness from operating lines of credit

Accoutns payable and accured liabilities

Refund liabilties

Deferred revenue

Sales and property taxse

Payroll

Notes payable

Current portion of bank loans and mortgages

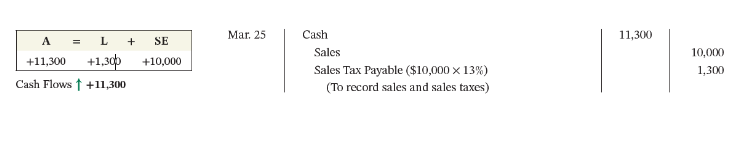

Sales taxes

Federal good and service tax (GST)

Povincial (PST, QST)

Combined in to one sometimes (HST)

Screen clipping taken: 2024-03-12 3:32 PM

Sales tax payable

May or may not be included in sale price

To calculate the sales portion

Divide the cash received by 100 percent plus the sales tax percentag

Screen clipping taken: 2024-03-12 3:32 PM

Must be remitted periodically to repective governments

When paid, debit sales tax payable accoutn and credit cash

Payroll

Salary

Payroll deductions required to be withheld from employees' gross pay

Emploee's froos pay less payroll deductions is known as net pay

Employee payroll deductions

Mandatory payroll deductions

Federal and provincal income taxes

Canada pension plan

Employment insurance

Voluntary payroll deductions

Benefits

Unions dues

Chartiable donations

Screen clipping taken: 2024-03-12 3:35 PM

Employee payroll liabilities

Employer's share of CPP and EI

Workers compensation

Employee benefits

Compensated adsences

Employer-sponsored health plans and pensions

Screen clipping taken: 2024-03-12 3:36 PM

Operating line of credit (credit facility)

Pre-arranged agreement between a company and a lender to allow the company to borrow up to pre-authorized limit whenever required

To help manage remp cash short falls

Company repays whatever portion of the borrowed funds it chooses whenever it is able to

Interest is shared using a floating or variable interest rate

Security (collateral) may be required by bank

When used, results in bank indebtedness; reported in current liabilites section of statement of financial position

Liabilities with principal due at maturity

A promise to pay a specified amoutn usually on a fixed future date

Often used instead of accounts payable

Formal written promise, provides stong legal claim

Bears interst at a fixed interest rate, which is constant for the entire term of the note

Issued for varying periods of time

If due within one year of financial statement date, classified as current liabilities

Liabilities with Instalment payments

Normally non-current liabilities

Obligations to be paid after one year or more

Bank loand payble, moergagse payable

Series of periodic payment, called instalments, consisting of

Interest on the unpaid balance of the loan at the beginning of the period

A repayment of the portion of the loan principal

A specified repayment schdule must be followed

Currents and non-current portions

For a loan reuiqring instalment payments, the principal portion of the loand that will be repaid durign the enxt is a current liability

Portion that will be repaid after the next year is non current liability

Other non-current liabilites include

Banks loans, notes and mortgages payable

Bonds payable

Lease liabilites

Deferred income taxes and pension liabilites

Statement Presentation

Current Liabilities

Reported as the first category of liabilities

Can be listed separtely on statement of financial position or detailed in the notes

Normally listed in order in which they are du

Non-current liabilities

Typically presented immediately following current liabilities and detail in notes

Generally measured and reported at amount expectd to be paid when due

Analysis of debt obligation

Liquidity- ratios measure short term ability to pay maturing obligation and meet unexpected cash needs within the next year

Current ratio

Inventory turnover

Receivables turnover

Solvency- ratios measure ability ro meet LT obligions

Debt to total assets

Times interst earned

Debt to total assets

Indicates the extent to which a company's assets are financed by debt

Debt to total assets= total liabilites/total assets

Lower is better

Times interest earned

Provides an indication of a company's ability to meet interest payments as they come due

Times interest earned = net income + interest expense+( income tax expense/interest expense)

No comments:

Post a Comment