Types of Receiveables

Amounts owed to a company by its customers, emplyoyees, government and others, considered financial assets

Claims that are expected to be collected in cash

Frequently classified as

Accounts receiavle -amounts owed by scustomers resulting from the sale of goods and services

Notes receibale - written promises to repay debt

a/r and n/r resulting from sales transactions are often referred to as trade receivables

Other receibables (nontrade receivables)

Do not result from the normal operations of th ebusiness

Interest receivable, loans to company officers and advanes to employees, sales tax recoverable, income tax receivable

Recording accounts receivable

A receivable is recorded when services is provided on account or at point os sale of merchandise on account

Initially recorded at the transaction price

A receivable is reduced by variable consideration such as expected sales returns and allowances and by sales discounts

Also reduced when payment is received or the merchandise is returned by the customer

Subsidiary Ledgers

The subsidiary ledger for accounts receivable provides the details that support the total balance for accounts receivable in the general ledger

The single accounts receivable account in the general ledger is the control account

The balance in the control account must always equal the total of all the individual subsidiary ledger accoutns (one for each customer) in the subsidiary ledger

Accounting for credit losses

Somes accoutns receivable become uncollectible

Expected credit losses are debited to an account called credit losses

Bsed on company's historical credit loss experiaence

Also called bad debt expense or impairment losses

Credit loss expense is recognized in the same period that the related sales revenue is reported.

Allowance Method

This method estimates the expected cdit losses at the end of each period

The amount estimated is shown in the allowance for expected credit losses (formerly allowance for doubtful accountants)

A contra asset acccount- normally with a credit balance

Shown below the netted with amounts receivable to determine the carrying amount

Not that the allowance is an estiamate - it does not show specific customer accounts

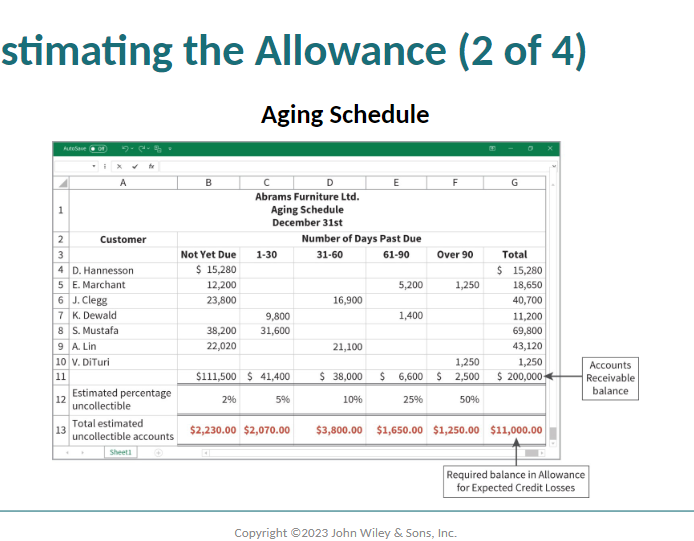

Estimating the Allowance

Most companies use the percentage of receivables basis to determine the allowance

Estimate the percentage of receivables that are likely to be uncollectible

Either one percentage that is applied to the entire accounts receivable balance or

Different percentages applied to accounts receivable that are classified accourding to the length of time they have been outstanding (called an aging of accounts receivable)

Screen clipping taken: 2024-02-26 7:35 PM

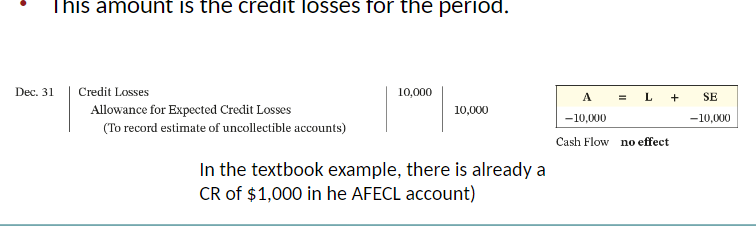

Once the appropriate estimate for uncollectible accounts is determined, an adjusting entry can be recorded

The amount of credit losses to be expensed in the period is the difference between the required balance and the exisitng balance in the allownace account

This amount is the credit losses for the period

Screen clipping taken: 2024-02-26 7:37 PM

Screen clipping taken: 2024-02-26 7:37 PM

Measuring and recording estimated uncollectible accounts

Credit losses are reported in the statement of income as an operating expense. The balance in the allowance for expected credit losses is deducted from accounts receivable in the current assets section of the statement of financial position

Screen clipping taken: 2024-02-26 7:40 PM

Screen clipping taken: 2024-02-26 7:40 PM

Screen clipping taken: 2024-02-26 7:42 PM

Recording the Recovery of an uncollectible account

An account prevously written off may be collected in the future- called a credit loss recovery

Record in 2 separate entreis

Reverse the write-off entry to retinstate the account, and

Record the cash collection

Screen clipping taken: 2024-02-26 7:45 PM

Screen clipping taken: 2024-02-26 7:51 PM

Summary of the allowance method

Measuring and recording estimated uncollectible account (credit loss entry)

Determined using a percentage of total or aged receivables

Any increase to the allowance is recorded as a debit to credit losses

Recording the write off of an uncollectible account (write off entry)

Actual accounts are written off when they are determined to be uncollectible

This write off reduces the allowance

Recording the recovery of an uncollectible account recorvery entries)

If a wirtten off account is later collected, the write off is reversed and the collection recorded

Account for notes receivable

Stronger legal claim to assets than accounts receivable; written promise to repay on demand (promissory note)

Credit instrument that normally

Requires the payment of interest

Extends for time periods greater than 30 days

Often used

When people and companies borrow money

When the amount and the length of credit period exceeds normal limits

To settle an accounts receivable when payment accnot be made within the established credit period

Screen clipping taken: 2024-02-26 7:56 PM

Screen clipping taken: 2024-02-26 7:56 PM

Screen clipping taken: 2024-02-26 7:56 PM

Derecognizing Notes receivable

Honoured- collected

Paid in full at maturity date

Collection recorded

Screen clipping taken: 2024-02-26 7:57 PM

Dishonoured

Not collected

Not paid at maturity date; note no longer negotiable

Balance transferred to accounts receivable if eventual collection expected

Balance written off to credit losses if eventual collection not expected

Dishonoured notes receivable

Screen clipping taken: 2024-02-26 8:00 PM

Screen clipping taken: 2024-02-26 8:00 PM

Statement Presntation

Statement of Financial position

Short term receivables reported in the current assets section

Following cash and trading investments

Reported at carrying amount, but must also disclose gross amount of receivable and the expected credit losses

Receibables due more than a year are presented sepately in the non-current assets section

Statement of income

Credit losses are reported as an operating expense

Interest income is reported in the non operating section as other icnomeand expenses

Managing Accounts Receivables

Determine to whom to extend credit to

Establish a payment period

If a customer does not pay within this period, and interest (financing) charge may be added to the amount due

Monitor collections

Prepare and update an accounts receivable aging schedule

Evaluate the liquidity of receivables

Evaluting the Liquidity of receivables

Liquidity is measured by how quickly certain assets can be converted into cash

Measures used to assess liquidity

Receivables turnover ratio

Average collection period

Receivables turnover

The number of times on average that receivables are collecteed during the year

Turnover = Credit Sales/ Average gross accoutns receivables

The higher the receiveables turnover ratio, the more liquid the company's receivables are

Average Collection Period

The average amount of time that a recievable is otuatanding

Average collection period= 365 days/ receivables turnover

The lower the average collection period, the more liquid the company's receivables are

Review of IFRS and ASPE

Wiley Chapter 8 Practice

No comments:

Post a Comment