Reporting and Analyzing Inventory

Determining Inventory quantities

Determining ownership o goods

Taking physical inventory, making count adjustments, internal controls

Inventory cost determination formulas

Spcific ID, FIFO, Average costs

Effects of cots formulas

Presentation and alalysis of inventory

Inventory costs formulas in a periodic system

Determining Inventory Quantities

Whether companies use a periodic or perpetual system, physical inventory must still be counted at the end of each accounting period

To check the accuracy of the perpetual inventory records

To determine the amount of inventory lost to shrinkage or theft

Determining Ownership

Ownership of goods must be considered when taking inventory

Goods in transit at the end of period determine of ownership more complicated

Determine who has legal title to good in transit

Include in inventory if company has legal title

Apply fright/shipping concepts from chapter 5

Ownership of cosigned goods remains with the owner (the consignor) not the holder of the goods

Goods taken home on approval by a customer are still owned by the company

Taking a Physical Inventory

To ensure inventory is properly counted, companies must ave a good system of internal control

Internal control systems include control activities, such as review and reconciliation

Counting inventory is a control activity

Allows reconciliation to information in a company's inventory system

Inventory Cost Formulas

Once inventory quantites are counte, must apply unit costs to determine total cost of inventory

Journal entries used to recrd purchaes of inventory only show the total costs, no the per unit cost

Units of the same inventory can be purchases at different prices

Which costs should be used?

Specific Identification

Tracks physical flow of goods

Each unit of inventory is tagged with is specific cost

Used in perperual system only

Can only be used where

Actual costs of each item can be determined

Goods are easily distinguishable

Goods can be produced and segregated for specific projets

Cost Formulas -FIFO and Average Cost

Cost formulas assume a flow of costs that may not be the same as the actual flow of goods

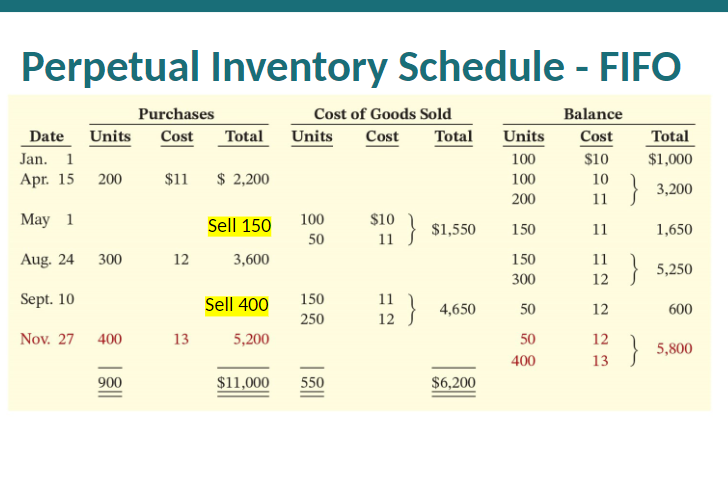

FIFO (First in First out)

Assumes that the earliest goods purchased are the first to be sold

Cost of first item purchases is costs of first item sold

Cost of ending inventory will be determined using the cots of the most recently purchased items

Average Cost

Cost is determined using a moving (wieghted) average of the unit cost of the items purchased

First in, First out (FIFO)

Merchandise inventory is recorded at most recent cost in the current assets seciton of statement of finacnal position

Cost of goods sold is recorded as an expense at oldest inventory cost on the statement of income

Ending inventor and cost of goods sold under FIFO are the same for periodic and perpetual inventory systems

Screen clipping taken: 2024-02-13 2:06 PM

Average Cost

Used when physical flow of inventory cannot pecifically be measured

Under a perpetual inventory system, a new eighted average unit cost is calculated after each purcahse

Used to record cost of goods sold and ending inventory

Screen clipping taken: 2024-02-13 2:08 PM

Choice of Inventory Cost Formula

Choose a formula that best

Represents as closely as possible the physical flow of goods

Reports ending inventory at recent costs

Use the same formula for inventories of similar nature and usage

Summary of Financial Statement Effects

Screen clipping taken: 2024-02-13 2:09 PM

Screen clipping taken: 2024-02-13 2:09 PM

Valuing inventory at the lower of cost and net realizable value

When the net realizable (fair) value is less than cost, the value is written down

Called the lower of cost and net realizable value LCNRV rule

Net realizable value NRV is selling price less any costs to make goods ready for sale

LCNRV Rule- Application

Apply rule to individual inventory intems

Reduce inventory by crediting it for the amount of write down debit is to cost of goods sold accoutn

Reverse write down if value subsequenctly recovers

When condition that caused the write down have changed

Reporting Inventory

In the statement of fianancial position

At the lower of cost and NRV

In the notes to the statements

Total amoutn of inventory

Costs of goods sold

Cost formulas used

Amoutn of write downs to NRV or reversals

Amoutn of any inventory pledged as security

No signigicant differences between IFRS and ASPE

Inventory turnover

How much inventory should a company have?

2 ratio to help manage

Inventory turn over ratio - measures the number of times, on average inventory is sold in a epriod

Days in inventory ratio convert inventory turnover ratio in number of days inventory is held

Inventory ratios

In general, the higher the inventory turnover and the lower the days in inventry ratios, the better

Inventory turnover= cost of goods sold/ average inventory

Days in inventory = 365 days/inventory turnover

No comments:

Post a Comment