Property, Plant and Equipment

Long0lived resources that

Are controlled by the company

Are tangible

Are used in the operation of a business

Are not intended for sale to customers

Provide economic benefits over many years

Reported as non-currents assets

Determining the Cost of Property, Plant and Equipment

Recorded at cost, which includes

Purchase price, including non-refundable taxes and duties, less discounts or rebates

Expenditures necessary to bring asset to its intended location and make it ready for its intended use

Estimated cost of future expenditures to dismantle, remove, or restore the asset at the end of its useful life

Usually subdivided into classes, such as land, land improvement, buildings, and equipment

Land

Cost of land includes

Purchase price

Closing costs such as survery, title search, and legal feeds

Additional costs to prepare land for its intended use (minus any proceeds from salvage)

Land has an unlimited life there it is not deprecaited

Land Improvements

The costs to structural additons made to a property

These decline in service potential over time

They are recorded separately from land

Depreciated over their useful lives

Does not include costs of getting the land ready to use

Equipment

All expenditres related to the purchase or construction of a building

When a buildingis prucahsed such costs include

Purcahse price

Closing costs

Costs required to make building ready for its intended use

When a building is contructed its cots consits of

Contract price

Archietects feeds

Building permits

Excation costs

Interest costs during construction

Equipemtn

Costs include

Purcahse price

Frieght charges, sales tax or cost of insurance during transit paid by the purchaser

Assumbling

Installing and tseting

Expenditures during useful life

After acqustion

Operating expenditures

Benefit only the current period

Required to maintain asset in normal operating conditions

Captial expenditures

Capitalized as an asset (increases the cost of the asset)

Increases life of an asset, its productivity or efficiency

Buy or Lease?

Advantages of leasing

Little or no down payment

Reduced risk of obsolesence

Csh outlays for asset (over time instead of up front)

100 percent financing

Income tax advantages

Terminology

Lessor

Owner of asset for lease (landlord)

Lessee

Party leasing asset from owner

IFRS Lease Rules

Lease is considered to be for an asset purchase financed with a loan proided by the lessor

Risk and rewards of ownership transfer to lessee even if legal title has not passed

Lessee is required to reported leased asset (as a right of use asset) and related liabilitiy

Exceptions where lease is treated a period expense are

Lease terms of less than 12 months

Leases for low value assets

ASPE Lease rules

2 types of leases

Capital lease

Substantially all benefits and risk of ownership are transferred from lessor to lessee

Lessee required to recordleased asset and related liability at present value of minimum lease payments

Operating lease

Benefits and risk of ownership not transferred to lessee

Lease (rental ) payments recorded as expensive by lessee and as revenue by lessor

Depreciation

Systematic allocation of the cost of property, plant, and equipment over the asset's useful life

A process of cost allocation, not determining an asset's current value

DOES NOT USE OR PROVIDE CASH to replacethe asset

Factors in calculating depreciation

Cost

Purchase price plus costs required to get the asset ready for use plus estimated asset retirement costs

Useful life

The time period that the asset is expected to be avilable for use, or

The numbr of uniters that the assets is ecpected to produce or the units of output value

Residual value

Estimated amount to be received from the disposal at the end of th asset's useful life

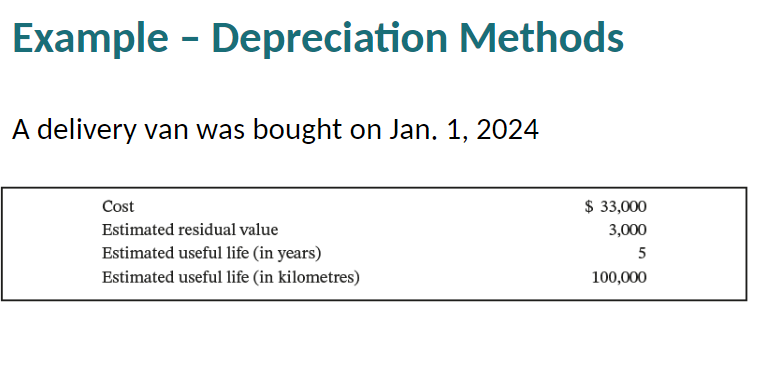

Depreciation Methods

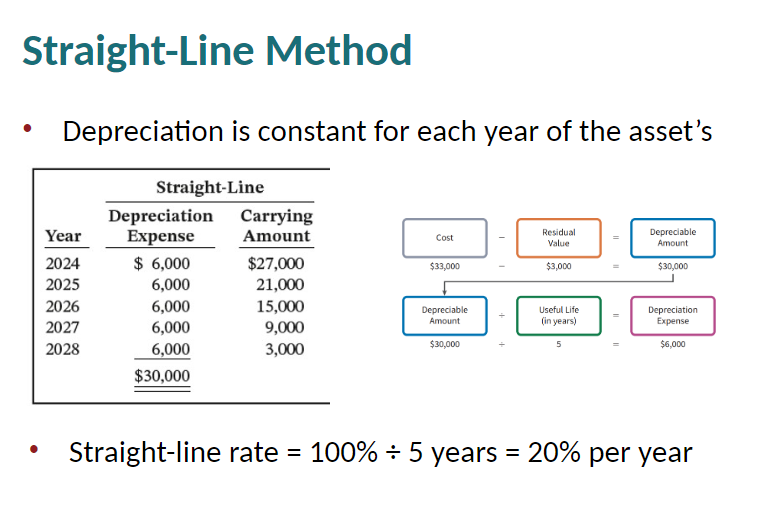

Straightline

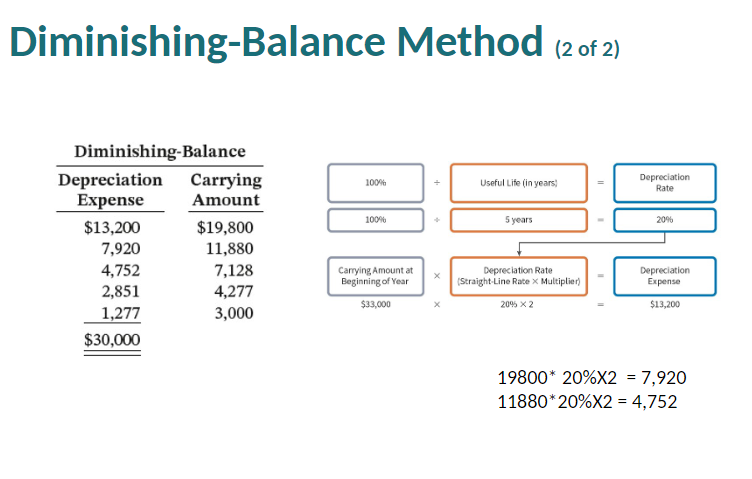

Diminsihing-balance

Units of produciton

Management chooses the method that best reflects the pattern of use of the ecnomic benefits from that asset

Screen clipping taken: 2024-03-06 4:57 PM

Straight line Method

Screen clipping taken: 2024-03-06 4:57 PM

Diminising- Balance method

Produces a decreasing annual depreciation expense over an asset's useful life

Depreciation is calculated based on the assets carrying amoung, which decline each year as accumulated depreciation increases

Annual depreciaiont expense is culaculated by multiplying the carrting amount at the beginning of the year by the depreciation rate

Resdiaul value is not included in the calculation-expceptin not for final year

Can be applied using different rates

Depreication rate = straight line line rate * multiplier

Screen clipping taken: 2024-03-06 4:59 PM

Unit of production method

Useful life is expressed in terms of total units of production or activity expected from the asset

Such as units produced or machine hours worked

Useful for factory machinery, vehicles, airplanes, or any asset whose usage varies over time

Screen clipping taken: 2024-03-06 5:00 PM

Screen clipping taken: 2024-03-06 5:01 PM

Other issues- revising depreciaiton

Revisions needed if

Change in estimated useful life or residual value

Capital expenditures (additions) during useful life

Impairment

Change in the pattern in which the asset's economic benefits are consumed

Accounted for as change in estimate

Change made in current and future years, but not to prior periods (prospective, not retrospective)

Other issues - Accounting for natural resources

Long lived tangible assets that are consumed physicall over time

Often called wasting assets

Depreciation of natural recources is called depletion

Units of production method is usually used

As productino can vary from year to year

Reserve values are the fiar value of the resources

Impairment will arise if reserve value < carrying amount

Screen clipping taken: 2024-03-06 5:43 PM

Screen clipping taken: 2024-03-06 5:44 PM

Presentation of long-lived assets

Statement of Financial position

Reported as non-current assets under headings:

Property, plant and equipment

Intangible assets

Goodwill

Disclose cost and accumulated depreciation (amortization) of each major class of assets

Either in statement or in notes

Disclose depreciation/amortization methods and useful lives or rates

Statement of income

Depreciation expense, amortization expense, gains and losses on disposal, and impairment losses are included in the operating expenses section

Statement of cash flows

Cash flows form the purcahse and sale of long-lived assets are reported in the investing section

Return on Assets

Measures overall posfitability

Return on Assets = Net income/ Average total assets

Higher is better because it indicates that for every dollar invested in assets, more net incoem is being generated

Asset turnover

Measures how efficiently a company uses its assets

Assets Turnover = Sales/ Average Total Assets

Higher is better because it indicates that for every dollar invested in assets, more sales are being generated

Profit Margin revisted

Together, profit margin and asset turnover explain the return on assets ratio

Profit margin * asset turnover = return on assets

Screen clipping taken: 2024-03-06 5:49 PM

Screen clipping taken: 2024-03-06 5:49 PM

No comments:

Post a Comment