Accrual Accounting Concepts

Accrual Accounting and the need for adjusting entries

Accrual vs cash basis of accounting

Revenue and expense recognition

Adjusting entries

Adjusting entries

Prepaid expenses, deferred revenues accrued expenses accured revenues

The adjusted trail balance and fiananical statements

Closing the book

Post closing trail balance

Accrual Accounting

Users require financial info on a regular basis

Accounting divides the economic life of a business into time periods

Year, quarter, month

One year period is known as the fiscal year

Shorter periods are known as interim periods

Many transactions affect more than one time period

Accrual Basis Accounting

Transactions affecting a company's financial statements are recorded in the period the events occur, rather than when cash is received or paid

Revenue is recorded when earned, even if the cash has not been received

Expenses are recorded when goods or services are consumed or used rather than when cash is paid

Cash Basis Accounting

Revenue is recorded only when cash is received

Expenses are recorded only when cash is padi

Can lead to misleading info decision-making

Timeing differences between the occurance of the actual event and its related cash flows

Revenue and expenses can be manipulated by timing the receipt and payment for cash

Revenue Recognition

Revenue

Increase in assets or settlements of liabilities

Results from a company's ordinary activities

In general revenue is recognized

Ina merchandising company when merchansidse is sold and delivered point of sale

Ina service company when the service is performed

Under ASPE revenue can be recognized when

Services have been proided or the risks and rewards of ownership of the goods have been transferred to the buyer

Revenue can be reliably measured

Collection is reaonably certain

Under IFRS revenues are recognized whena company satisfies a performance obligation

Five step process to measure and report revenue

Identity the contract with the cilent or customer

Identify the perfomance obligations in the contract

Determine the transaction price

Allocate the transaction price to the performance obligaiton in the contract]

Recognize revenue when or as the company satisfies the performance obligation

Expense Recognition

Expenses are recognized recorded when a decrease in economic rsrouces occurs

Assets are consumed they decrease or libailites are incurred they increase

Due to a company ordinary revenue genrating actilites

Tied to changes in assets and liabilites

Often coincides with revenue recognition

Recognized whenever possible in the period in which effort is made to generate revenue

Sometimes known as matching

Need for Adjusting entires

Entries made at the end of the accounting period to update accounts and produce up-to-date relevant financial info

Required because the trail balance may be not complete and up to date

Some events are recorded daily

Some costs are not included during the accounting period as they expire due to the passage of time

Some times may be unrecorded because their amounts are not known

Types of Adjusting Entries

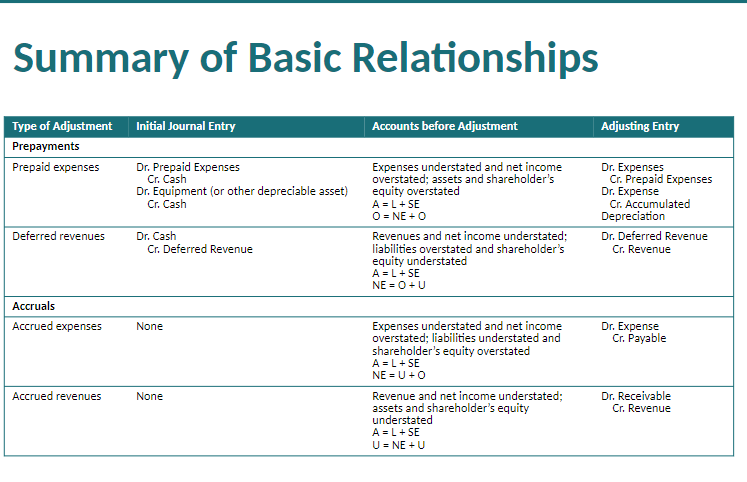

Prepayments

Preaid expenses

Deferred revenues

Accurals

Accrued expenses

Accrued revenues

Prepaid Expenses

When expenses are paid before they are used or consumed, an asset is recorded

When expenses are prepaid , an asset(prepaid expenses) is increased, debited to shows the future service or benefit and cash is decreased, credited

Expire with the passage of time or though use

Not practical to record is expiration on a daily basis, so done periodically, usually when statements are prepared

Adjusting entry increases (debits) an expense account and decreases( credits) the asset, prepaid account

Deferred Revenues

Cash received from customers before goods or services are provided to them

Revenues not recorded as it has not yet been earned

Recorded as a liability to recognize the performance obligations

When the cash is received, cash is increased (debited) and a liability account (deferred revenue) is increased (credited)

The opposite of prepaid expenses

Ajusting entry decreases the liability (deferred revenue) accounting and increases a revenue accounting to record revenue earned

Accrued Expenses

Any expeses that have been incrred that have not yet been recorded during the accounting period

Adjustments make for accrued expnnses to record obligations that exist at the end of th eperiod and to recognize expenses that have been incurred during the current accounting period

Adjusting entry results in an increase (debit) to an expense account and n increase (credit) to a liability (payable) account

Accrued Revenues

Revenues that have been earned but not yet recorded at the end of an accounting period

Adjustment is required to record the receivable that exists at the end of the period and to record the revenue that has been earned during the period

Adjusting entry results in an increase (debit) to an asset accounting and an increase (credit) to a revenue account

Screen clipping taken: 2024-01-30 9:15 PM

Adjusted Trail Balance

Prepared after alladjusing entries have been recorded and posted

Shows the balcnes of all acounting at the end of the accounting period, cluding those accounting that have been adjusted

Proves total debit balances and total credit balances are equal after the adjusting entires have been made

The main source for prep of financial statements

Financial statements

Prepared in the following order

Statement of income is prepped first using revenue and expense accounts

Statement of changes in equity using equity accounting and net income from the income statement

Statement of financial position is prepared third, using asset, liability and equity accounts

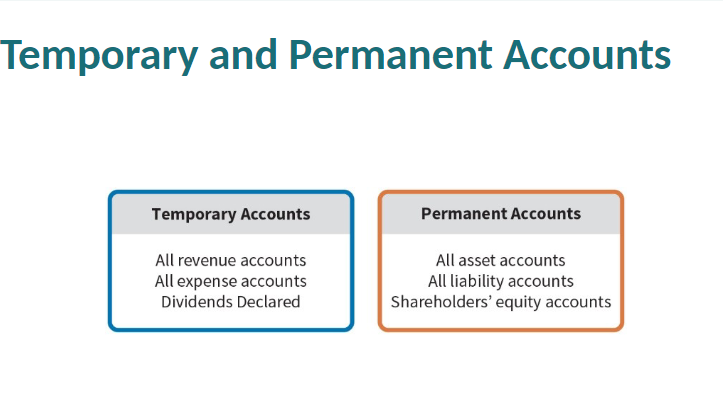

Closing Entries

Revenue, Expense and dividends declared accounts are components of retained earning

Considered to be temp accounts

Statement of financial position accounting carry forward into the future

Considered to be perma accounts

Closing entries

Temp accounting balances transferred to retained earnigns

Produce a zero balance in the temp accounts to prepare them for the next period's activity

Screen clipping taken: 2024-01-30 9:20 PM

The Closing Process

Close all revenue accounts

Debit each revenue account for its balance and credit income

Summary for total revenue amount

Close all expense accounts

Debit income summary for the total expense amount and credit each expense account for its balance

Close income summary

Debit or credit income summary for the balance in the account and credit (debit) retained earnings

Close Dividends declared account

Debit retained earning and credit dividends declared account for the balance

Screen clipping taken: 2024-01-30 9:24 PM

Post-closing trail balance

Lists all perma accounts and their balances after all closing entreis are jounalized and posted

Proves that total debit balances and total credit balances are equal after the closing entries have been jounalized and posted

No comments:

Post a Comment